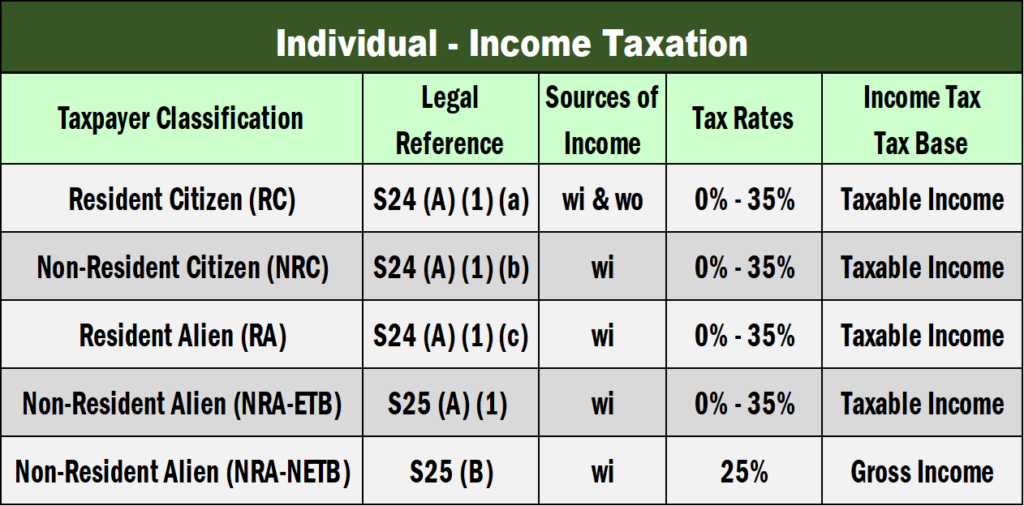

- Resident

- Citizen / Estate / Trust

- Alien

- Non-Resident

- Citizen

- Alien

- Engaged in Trade or Business

- Not-Engaged in Trade or Business

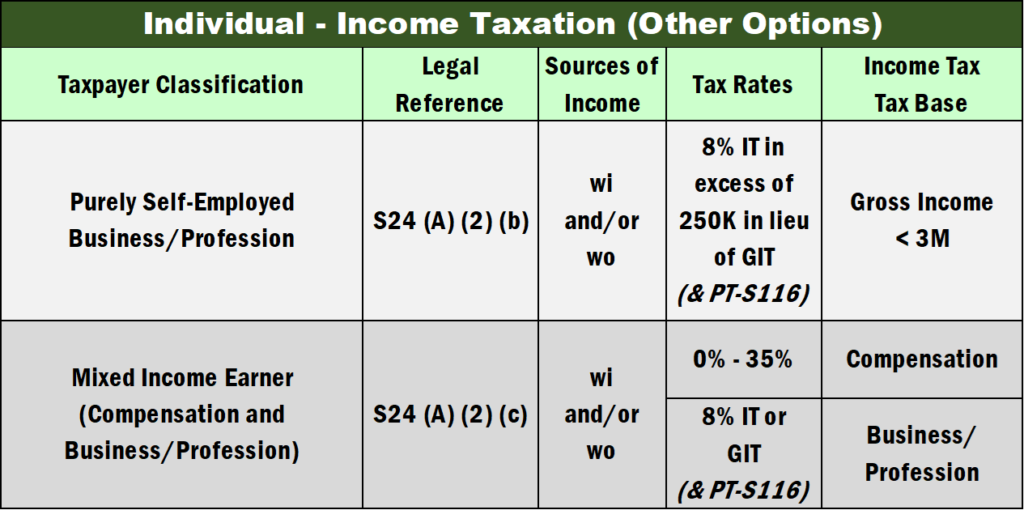

- Graduated income tax on individuals and 8% IT option

- Capital gains tax of an individual on sale or exchange of shares of stocks classified as capital assets.

- Capital gains tax on sale or exchange of real properties classified as capital assets

- Final Tax on certain passive income paid to residents

- Final Tax income of Non-Resident aliens

- Final Tax on special individuals

- Fringe benefit tax on fringe benefits of supervisors and managers payable by employer.

NRC – Non-Resident Citizen

Period of stay of contract worker abroad is 183 days or more

NRAETB – Non-Resident Alien Engaged in Trade or Business

Period of stay in the Philippines during any taxable year exceeds 180 days

NRANETB – Non-Resident Alien NOT Engaged in Trade or Business

Period of stay in the Philippines during any taxable year does not exceed 180 days

Income Tax Rate Options for Individual Taxpayer

- 8% Income Tax option

- Based on Gross Income

- Graduated Income Tax option - based on a Graduated Income Tax Table

- Optional Standard Deduction

- Allowed Itemized Deduction

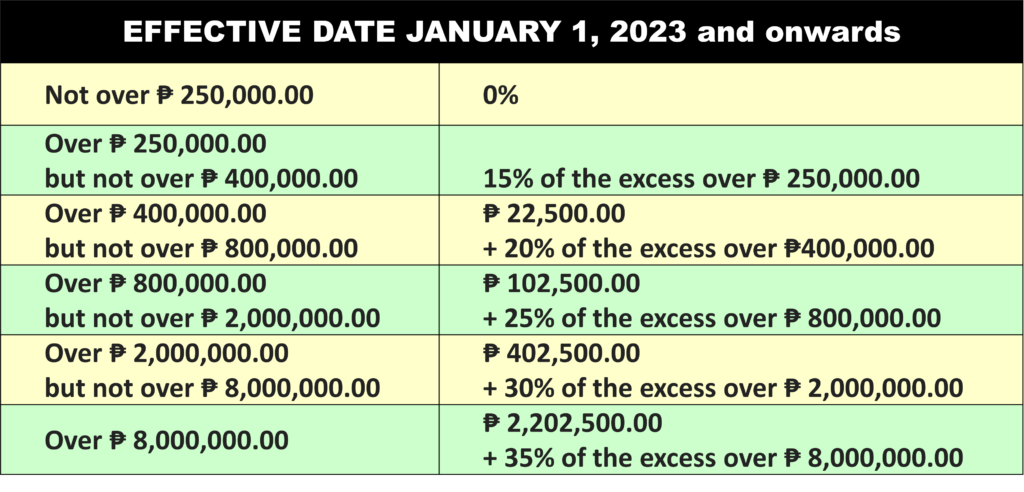

Graduated Income Tax Table