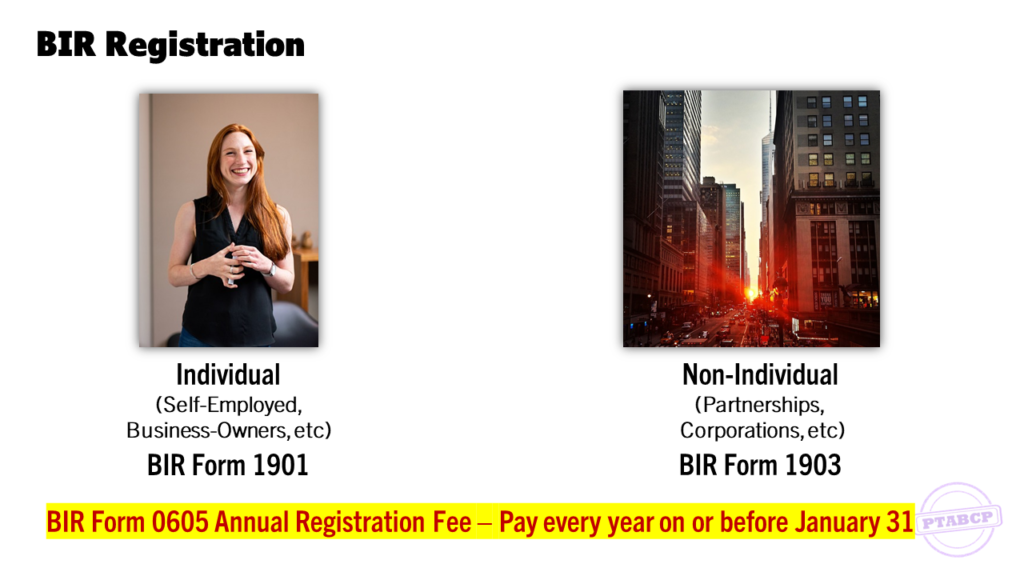

Accommodation Service Business can be operated by Individual or Non-Individual Entities. Being so, they must register their accommodation service business with the Bureau of Internal Revenue (BIR)

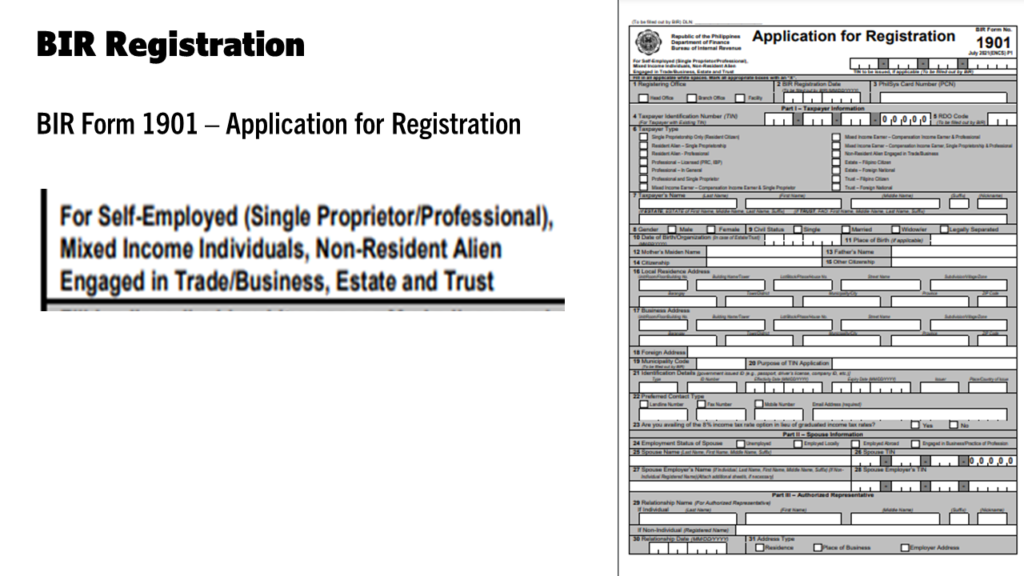

BIR Registration for Individual

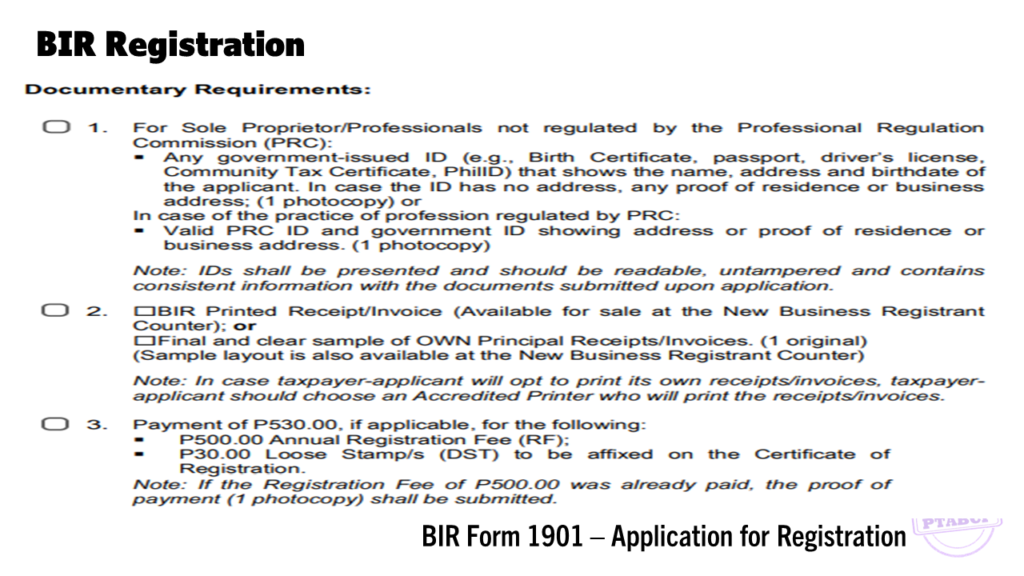

- Accomplish BIR Form 1901

- Attach Documentary Requirements

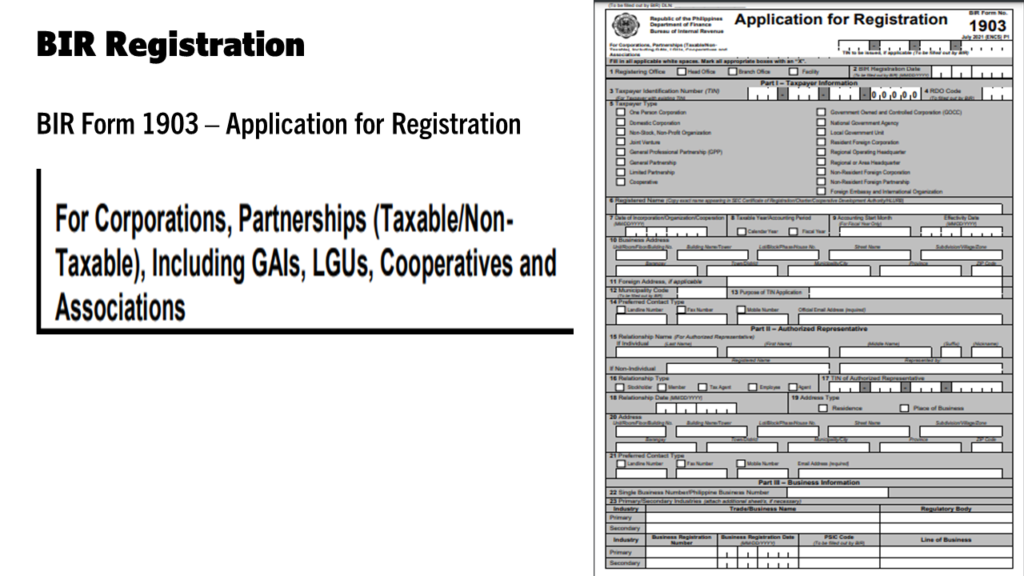

BIR Registration for Non-Individual

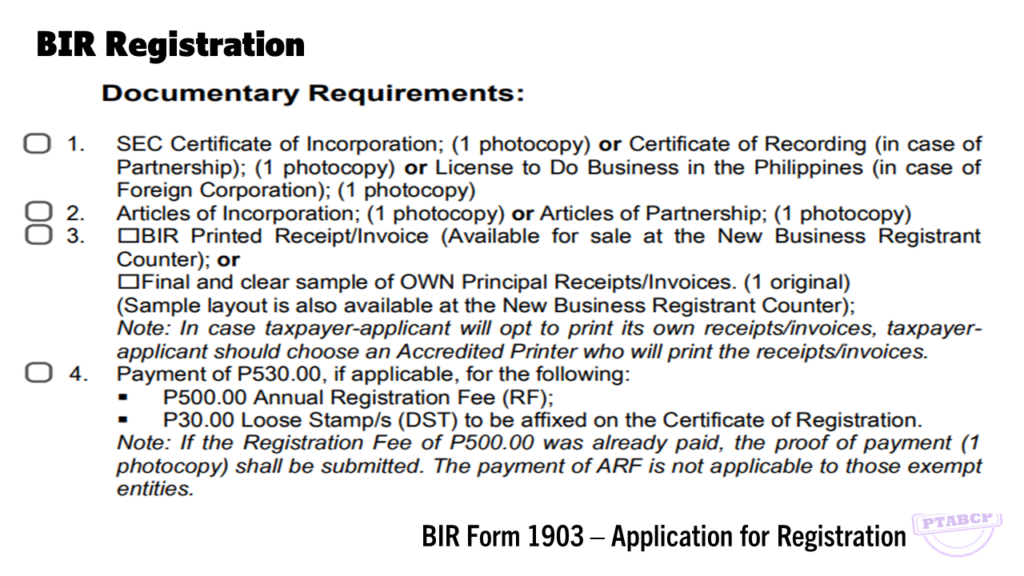

- Accomplish BIR Form 1903

- Attach Documentary Requirements

Register and Keep Books of Accounts

The National Internal Revenue Code (NIRC) mandates that a Taxpayer (TP) shall keep Books Of Accounts.

Keeping of Books of Accounts

Legal Basis:

Sec.232 (A), NIRC, as amended. Corporations, Companies, Partnerships or Persons Required to Keep Books of Accounts. - All corporations, companies, partnerships or persons required by law to pay internal revenue taxes shall keep and use relevant and appropriate set of bookkeeping records duly authorized by the Secretary of Finance wherein all transactions and results of operations are shown and from which all taxes due the Government may readily and accurately be ascertained and determined any time of the year.

Provided, that corporations, companies, partnerships or persons whose gross annual sales, earnings, receipts or output exceed Three Million pesos (P3,000,000), shall have their books of accounts audited and examined yearly by independent Certified Public Accountants and their income tax returns accompanied with a duly accomplished Account Information Form(AIF) which shall contain, among others, information lifted from certified balance sheets, profit and loss statements, schedules listing income-producing properties and the corresponding income therefrom and other relevant statements

Thus, a Taxpayer shall apply and register for Books Of Accounts (BOA) with the Bureau of Internal Revenue (BIR), the only body which has authority over Books Of Accounts

===

What Books Of Accounts must be registered with the BIR?

Gross Receipts

Per Sec. 2 (g), RR 8-2018; Jan 25, 2018

Refers to the total amount of money or its equivalent representing contract price, compensation, service fee, rental or royalty, including the amount charged for materials supplied with the services, and deposits and advance payments actually or constructively received during the taxable period for the services performed or to be performed for another person, except returnable security deposits for purposes of these regulations.

In the case of VAT taxpayer, this shall exclude the VAT component

Gross Receipts - Hotel, motel, rest/pension/lodging house and resort operators

Republic Act No. 11360

AN ACT PROVIDING THAT SERVICE CHARGES COLLECTED BY HOTELS, RESTAURANTS AND OTHER SIMILAR ESTABLISHMENTS BE DISTRIBUTED IN FULL TO ALL COVERED EMPLOYEES, AMENDING FOR THE PURPOSE PRESIDENTIAL DECREE NO. 442, AS AMENDED, OTHERWISE KNOW AS THE “LABOR CODE OF THE PHILIPPINES”

Art. 96. Service Charges. – All service charges collected by hotels, restaurants, and similar establishments shall be distributed completely and equally among the covered workers except managerial employees.

In the event that the minimum wage is increased by law or wage order, service charges paid to the covered employees shall not be considered in determining the employer’s compliance with the increased minimum wage.

Supreme Court (SC) decision regarding deductions

When a taxpayer claims a deduction, he must point to some specific provision of the statute in which that deduction is authorized and must be able to prove that he is entitled to the deduction which the law allows. An item of expenditure, therefore, must fall squarely within the language of the law in order to be deductible.

Cost of Service

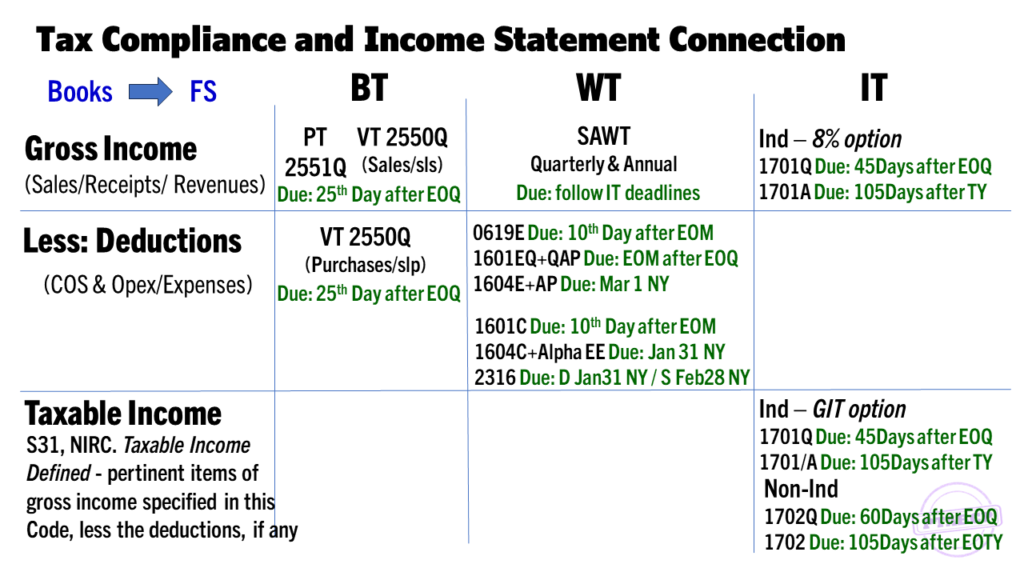

Business Tax comes in two forms:

- Percentage Tax, or

- Value Added Tax

Withholding Taxes - Sec.58(A), NIRC

- A manner or system of collecting taxes with the end in view of collecting in advance the full amount of tax or at least the approximate tax due from the payee on certain income payments

- The amount withheld is a special trust fund in trust for the government until paid or remitted by WA to BIR

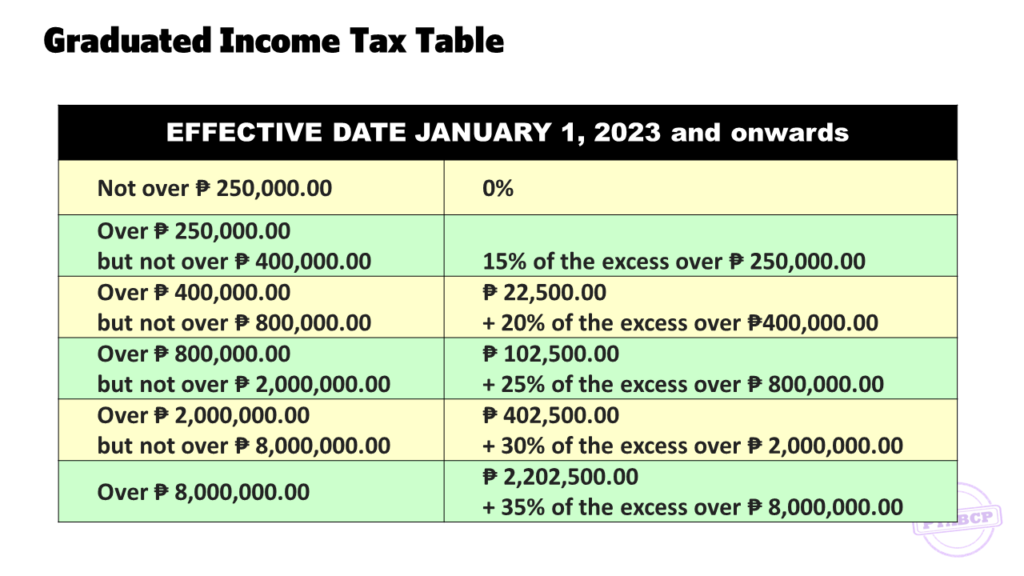

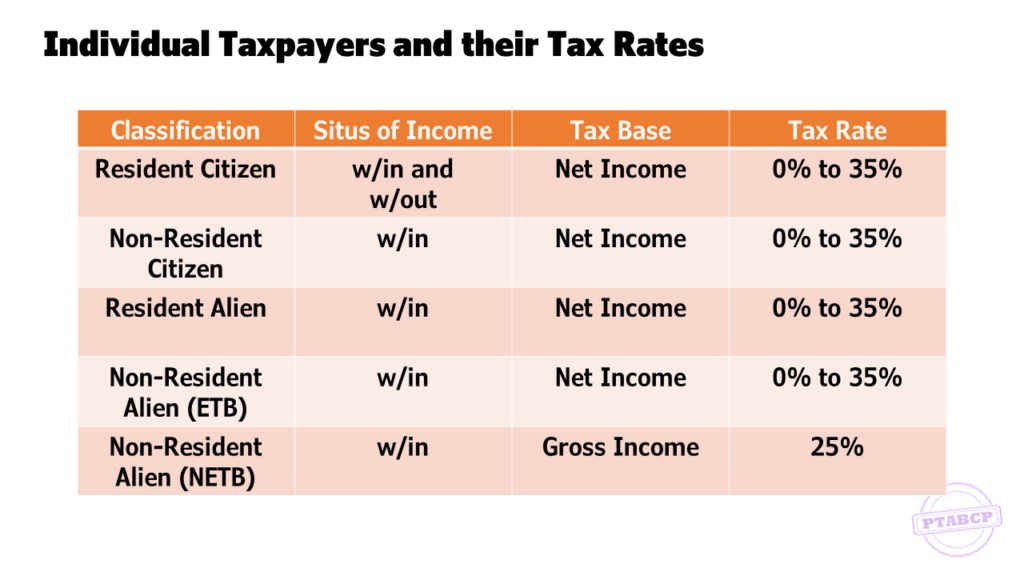

INCOME TAX RATES FOR INDIVIDUALS

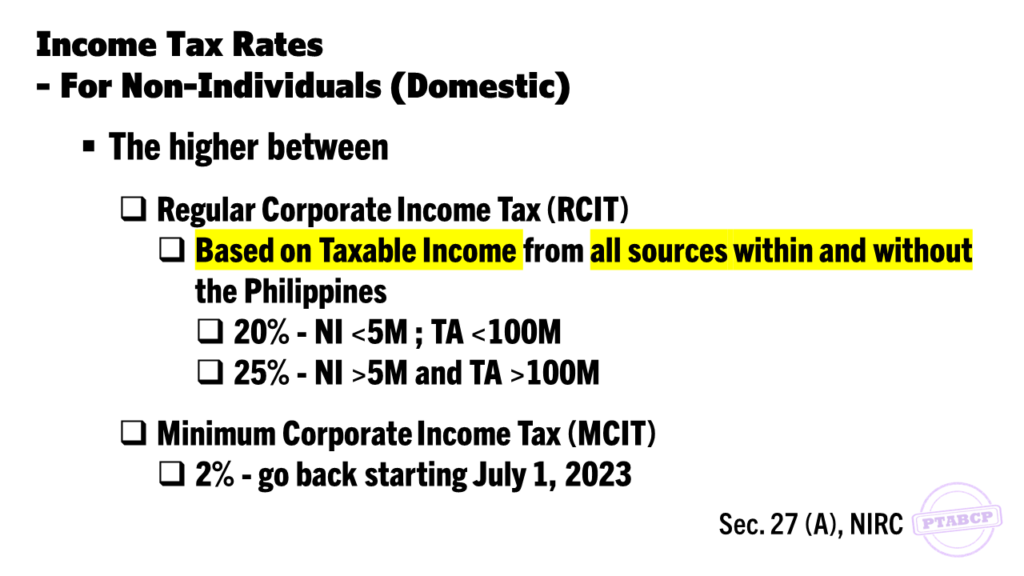

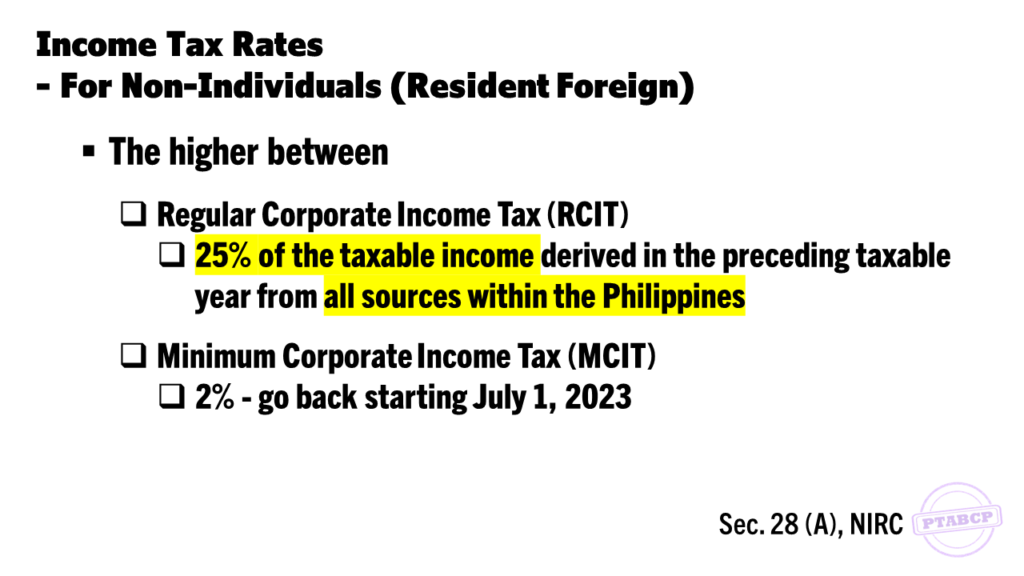

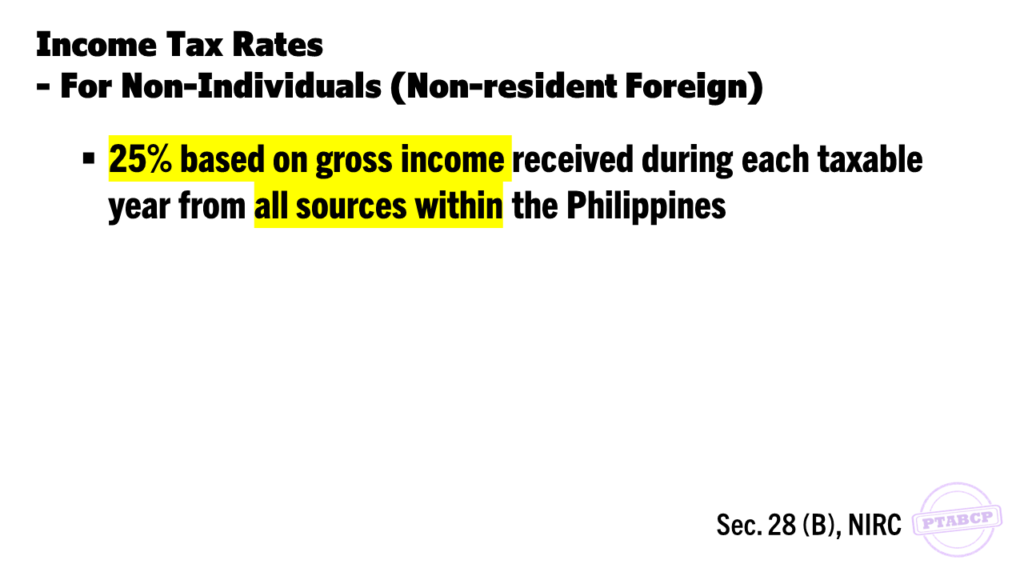

INCOME TAX RATES FOR NON-INDIVIDUALS